In Short

The first quarter of 2026 round-tripped. Prices fell sharply at the onset of U.S. military action against Iran and recovered by mid-April, but the operating environment for companies looks materially harder for the next year on higher inflation, higher oil prices, and higher debt costs. AI is a wildcard that is particularly hard to forecast today.

Macro Commentary

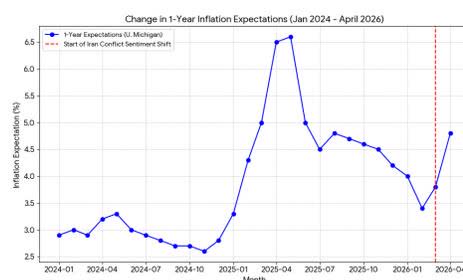

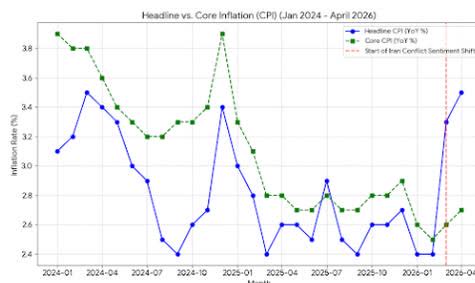

The US consumer continues to be surprisingly resilient in the face of higher costs. Even while many of last year’s tariffs were removed in February, inflation and inflation expectations are increasing again as the prospect of a global oil shortage begins to have an impact.

We believe that the economy is ultimately the product of the cost of energy, the cost of capital, and the prevalence of employed citizens, with productivity gains as a wildcard of smaller import.

American military action against Iran has had a significant and negative near term impact on the price of energy. This is somewhat offset in the United States as it benefits the oil producing regions, but it is still likely to result in higher inflation for the US consumer. The stock market has accepted this outcome with little fanfare given its assumption that oil prices will normalize in relatively short order. We are more cautious and believe normalization in oil prices will take longer than the market seems to assume.

With oil prices higher, inflation is more likely to embed into the cost of goods. We expect the Federal Reserve to take longer to cut interest rates and for the cut rates to be less significant than the two, 25 basis points cuts the market assumes for 2026. Complicating that math is the Federal Reserve Chair nominee’s expressed desire to cut rates irrespective of evidence. We find it difficult to foresee a situation where that is prudent, yet short term rates are set by fiat and counterintuitive outcomes are therefore possible – adding to the difficulty in forecasting the future. Left to its own devices, the cost of capital should be higher than it would have been.

At the same time, artificial intelligence advances, now led by Anthropic’s Claude and Google (GOOG)’s Gemini with OpenAI’s ChatGPT trailing, continue, and have begun to become truly helpful to knowledge workers. While there may be an argument that increased access to coding will lead to transformative use cases that then require more coders, our view is that that is not true of every industry. In finance, for instance, where tools are now useful, our thought piece Career Advice for Aspiring Investment Management Analysts and Interns has gone from a likely scenario to one that is cheaper to implement than envisioned and is beginning to widely occur. While there is scant evidence that AI advancements have led to widespread job loss so far, employment gains have also not occurred, and we’re in the early innings of AI adoption. We believe there’s downside risk to employment.

The problem, at least as it regards AI, is that the truth is difficult to discern. Early leaks suggest Anthropic’s new model codenamed Mythos is more myth than mythological, with rumors of its new capabilities are more modest than the public has been led to believe. With both Anthropic and OpenAI planning IPOs this year, and planning to place significant portions directly with generally less critical retail investors, the gap between marketing and capability is large, and it’s prudent to treat the news flow with skepticism.

The AI supply chain, usually a good place to discern the truth, is an equally difficult space to understand, currently. On one hand Nvidia (NVDA) has a dominant technology with leads in hardware that’s locked by advantaged software that ensures that it’s multiple years ahead of the competition; on the other, all of the top cloud compute providers have also contracted with the likes of AMD (AMD), Broadcom (AVGO), Intel (INTC), and Marvell Technology (MRVL) to provide alternative chipsets. On one hand, the memory oligopoly argues that chip demand is so vast that we are severely memory constrained and are pricing out new phone and computer manufacturers orders; on the other, Google released a new process that should lower compute memory requirements by 80% and speed up inference workloads by 800%. On one hand, new chip production is set to come online over the next year that will significantly reduce bottlenecks; on the other, helium production, a key input in making chips, has been significantly set back by the global oil shortage. There’s a lot going on, and in today’s world, given the profit motives, it’s exceptionally difficult to differentiate signal from noise in the AI space.

Individual Stock Updates:

Icon Public Limited Company (ICLR) ($ICLR) is a global contract drug manufacturing company we’ve followed for some time but was always too well priced to own. In February, the company disclosed an internal investigation into revenue recognition that would impact revenue by less than 2%. The stock fell 40%. We like the fundamentals of the contract drug manufacturing industry and ICON’s record $24+ billion backlog. Previous to the restatement the company had the opportunity to address its cost structure even while being well positioned in the high-growth oncology and GLP-1/obesity therapeutic segments. We don’t believe the restatement should impact their margin opportunity, their existing contracts, or their ability to win new business and anticipate a significant rally after their formal restatement filing and funds again feel like they can “trust the numbers.” We believe the company trades at a low double digit multiple of free cash flow, a fraction of its historical average and a price that materially underestimates the strength of their business.

Perma-Fix Environmental (PESI) ($PESI) is a hazardous waste disposal company in the early days of a J-curve in revenue growth. Their most significant near term opportunity is the disposal of nuclear waste at their Hanford plant. On their last earnings call they announced the start of their ramp was delayed a quarter. This $200 million market capitalization company with $60 million in revenue will add $1-2 million per month in revenue to grout low activity nuclear waste in the next year as the disposal ramps to at least $70 million per year for the next 10 years. Additionally, there is an additional opportunity to earn a piece of an additional $4 billion in work currently being evaluated and awarded by the Department of Energy where Perma-Fix has the only regional facility to support the contract.

Another option for increased growth is the company’s second, fledgling business. The company has the ability to either earn their cost of capital on their next generation PFAS chemical destruction facilities (so called “forever chemicals”), or to sell or wind down the effort. The Company believes that their technology destroys PFAS more economically, more safely, and with fewer byproducts than its leading competitors. The division’s revenue is minimal to date, it has been a significant (for PESI) use of capital, and has significantly underperformed initial expectations. If this effort also inflects, as the company believes it will in the next year, the upside for the stock will be remarkable. If it doesn’t, the effort should be shut down – shortening the time to Perma-Fix’s cash flow breakeven, increasing the company’s return on capital, and supporting the stock’s upside.

S&P Global (SPGI) ($SPGI) is one of the financial market’s greatest toll businesses. White Brook bought a position during the first quarter when one of the quarter’s AI driven market sell-offs drove the price from >$550 to ~$380 on the speculation that artificial intelligence will destroy its moat. In reality growth and tumult in private credit, data center financing, and AI driven financial engineering products reinforce the necessity of the company’s services as a provider of ratings, analytics, and insight. While a stable or declining interest rate environment is more favorable for corporate bond issuance and refinancings to benefit the ratings division, the Company’s energy and commodities division will continue to prosper as companies consider new investment. We believe the company is a rare combination of defensive resilience and high-growth potential and are thrilled by the price that we were able to buy it.

Sanara Medtech (SMTI) ($SMTI) continues to be an extremely favorable risk reward. On their fourth quarter call they offered revenue guidance of 13-17% growth in line with sell side expectations but below the 20% some hoped for. At their valuation, we believe the forecasted growth to be more than good enough and likely to be revised upward. Perhaps underappreciated is that Sanara’s products are largely distributed by third parties who, to be effective, need to be at a hospital for a procedure – to ensure Sanara’s products are used. The more doctors who use their product at a specific location, the more reliably distributors show up to distribute their products. With increasing evidence of their product’s efficacy recently released and a focus on increasing per hospital doctor penetration, we continue to believe that there is significant room for sustained growth rate acceleration.

Negatively, Chemo Mouthpiece, their JV with InfuSystem did not receive upgraded coding from CMS under the durable medical equipment payment structure. While the subsidiary is well capitalized and is likely to press on, that upside option is likely a much smaller opportunity, and may be impaired. Hopefully it closes the book on the old management team’s efforts. We continue to believe the upside present is a multiple of the current share price and that the company is now exceptionally well led.

Rapid Micro Biosystems (RPID) ($RPID) also continues to be an extremely favorable risk reward. On their fourth quarter call, similar to last year, they also offered underwhelming guidance. The reasons given were that there can be no assurance that a new large deal can be won this year and that the large contract they are executing on ends, in part in February 2027, not December 2026, and therefore more machines than hoped might slip into the next calendar year. We believe guidance to be conservative given increasing business momentum with significant early rollouts with Amgen (AMGN), Samsung Biologics (SAMBF), and Merck Millipore (MKGAY) – all of which have capacity and are likely to place large follow-on orders. We also believe the company has good line of sight to increased gross margin upside starting in 2Q’26 when their new vendor agreements kick in. We believe management is exceptionally conservative, the company is well positioned, and the company represents the best risk reward in the portfolio.

We believe that each of these stocks will be meaningful contributors to performance in 2026 with news beginning to trickle in over the second quarter and significant progress reported by the third.

As always, feel free to reach out to discuss this or any of your investments at White Brook Capital. Fact sheets are available at Strategies – White Brook Capital. We continue to have confidence in all our strategies and are pleased with year to date activity. Specific client portfolio performance can be found in your quarterly statement.

Sincerely,

Basil F. Alsikafi

Portfolio Manager

White Brook Capital, LLC

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here